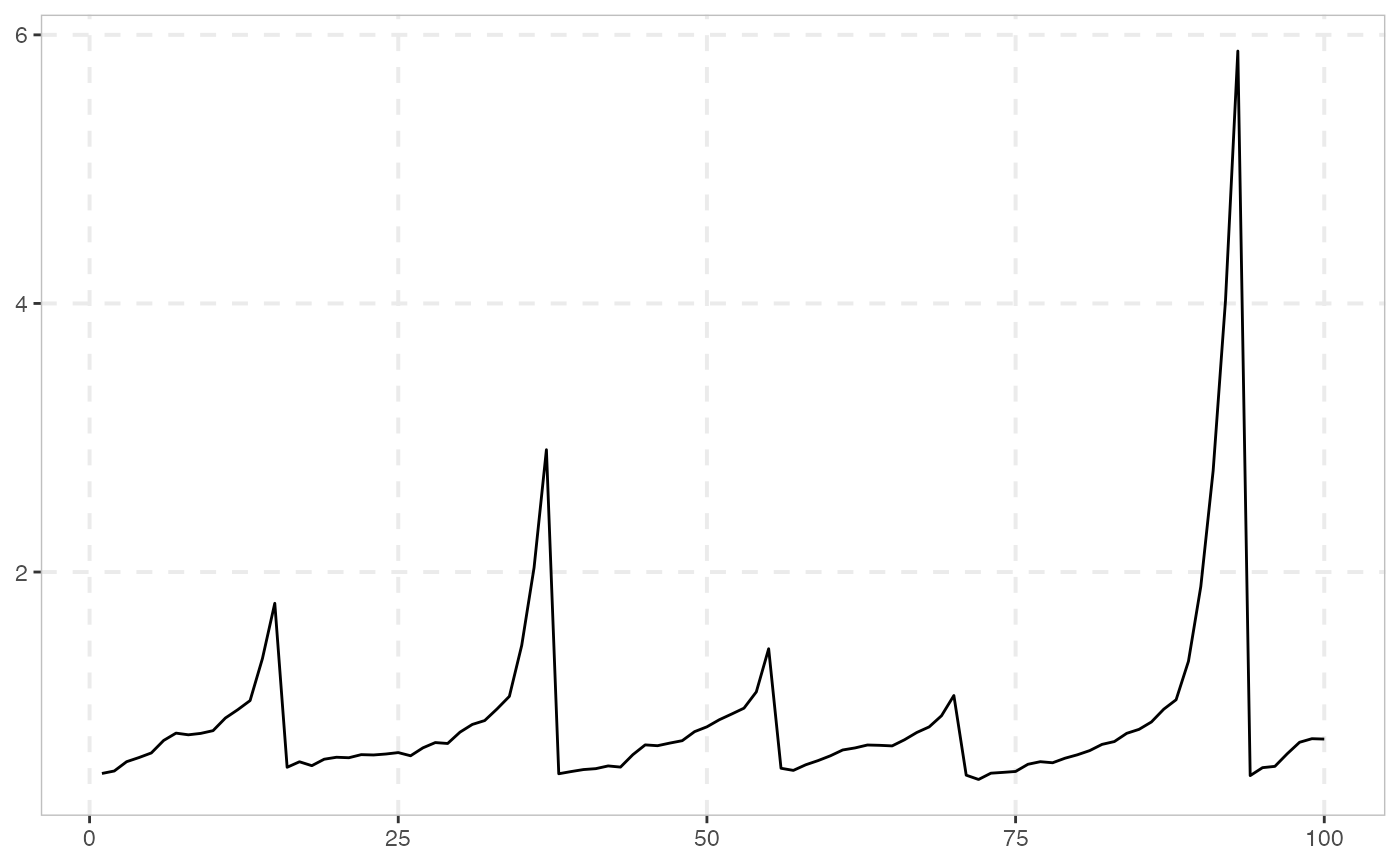

Simulation of an Evans (1991) rational periodically collapsing bubble process.

sim_evans(

n,

alpha = 1,

delta = 0.5,

tau = 0.05,

pi = 0.7,

r = 0.05,

b1 = delta,

seed = NULL

)Arguments

- n

A positive integer specifying the length of the simulated output series.

- alpha

A positive scalar, with restrictions (see details).

- delta

A positive scalar, with restrictions (see details).

- tau

The standard deviation of the innovations.

- pi

A positive value in (0, 1) which governs the probability of the bubble continuing to grow.

- r

A positive scalar that determines the growth rate of the bubble process.

- b1

A positive scalar, the initial value of the series. Defaults to

delta.- seed

An object specifying if and how the random number generator (rng) should be initialized. Either NULL or an integer will be used in a call to

set.seedbefore simulation. If set, the value is saved as "seed" attribute of the returned value. The default, NULL, will not change rng state, and return .Random.seed as the "seed" attribute. Results are different between the parallel and non-parallel option, even if they have the same seed.

Value

A numeric vector of length n.

Details

delta and alpha are positive parameters which satisfy \(0 < \delta < (1+r)\alpha\).

delta represents the size of the bubble after collapse.

The default value of r is 0.05.

The function checks whether alpha and delta satisfy this condition and will return an error if not.

The Evans bubble has two regimes. If \(B_t \leq \alpha\) the bubble grows at an average rate of \(1 + r\):

$$B_{t+1} = (1+r) B_t u_{t+1},$$

When \(B_t > \alpha\) the bubble expands at the increased rate of \((1+r)\pi^{-1}\):

$$B_{t+1} = [\delta + (1+r)\pi^{-1} \theta_{t+1}(B_t - (1+r)^{-1}\delta B_t )]u_{t+1},$$

where \(\theta\) theta is a binary variable that takes the value 0 with probability \(1-\pi\) and 1 with probability \(\pi\).

In the second phase, there is a (\(1-\pi\)) probability of the bubble process collapsing to delta.

By modifying the values of delta, alpha and pi the user can change the frequency at which bubbles appear, the mean duration of a bubble before collapse and the scale of the bubble.

References

Evans, G. W. (1991). Pitfalls in testing for explosive bubbles in asset prices. The American Economic Review, 81(4), 922-930.