radf_sb_cv computes critical values for the panel recursive unit root test using

the sieve bootstrap procedure outlined in Pavlidis et al. (2016). radf_sb_distr

computes the distribution.

radf_sb_cv(data, minw = NULL, lag = 0L, nboot = 500L, seed = NULL)

radf_sb_distr(data, minw = NULL, lag = 0L, nboot = 500L, seed = NULL)Arguments

- data

A univariate or multivariate numeric time series object, a numeric vector or matrix, or a data.frame. The object should not have any NA values.

- minw

A positive integer. The minimum window size (default = \((0.01 + 1.8/\sqrt(T))T\), where T denotes the sample size).

- lag

A non-negative integer. The lag length of the Augmented Dickey-Fuller regression (default = 0L).

- nboot

A positive integer. Number of bootstraps (default = 500L).

- seed

An object specifying if and how the random number generator (rng) should be initialized. Either NULL or an integer will be used in a call to

set.seedbefore simulation. If set, the value is saved as "seed" attribute of the returned value. The default, NULL, will not change rng state, and return .Random.seed as the "seed" attribute. Results are different between the parallel and non-parallel option, even if they have the same seed.

Value

For radf_sb_cv A list A list that contains the critical values

for the panel BSADF and panel GSADF test statistics. For radf_wb_dist a numeric vector

that contains the distribution of the panel GSADF statistic.

References

Pavlidis, E., Yusupova, A., Paya, I., Peel, D., Martínez-García, E., Mack, A., & Grossman, V. (2016). Episodes of exuberance in housing markets: In search of the smoking gun. The Journal of Real Estate Finance and Economics, 53(4), 419-449.

See also

radf_mc_cv for Monte Carlo critical values and

radf_wb_cv for wild Bootstrap critical values

Examples

# \donttest{

rsim_data <- radf(sim_data, lag = 1)

# Critical vales should have the same lag length with \code{radf()}

sb <- radf_sb_cv(sim_data, lag = 1)

tidy(sb)

#> # A tibble: 3 × 3

#> id sig gsadf_panel

#> <fct> <fct> <dbl>

#> 1 panel 90 0.356

#> 2 panel 95 0.451

#> 3 panel 99 0.637

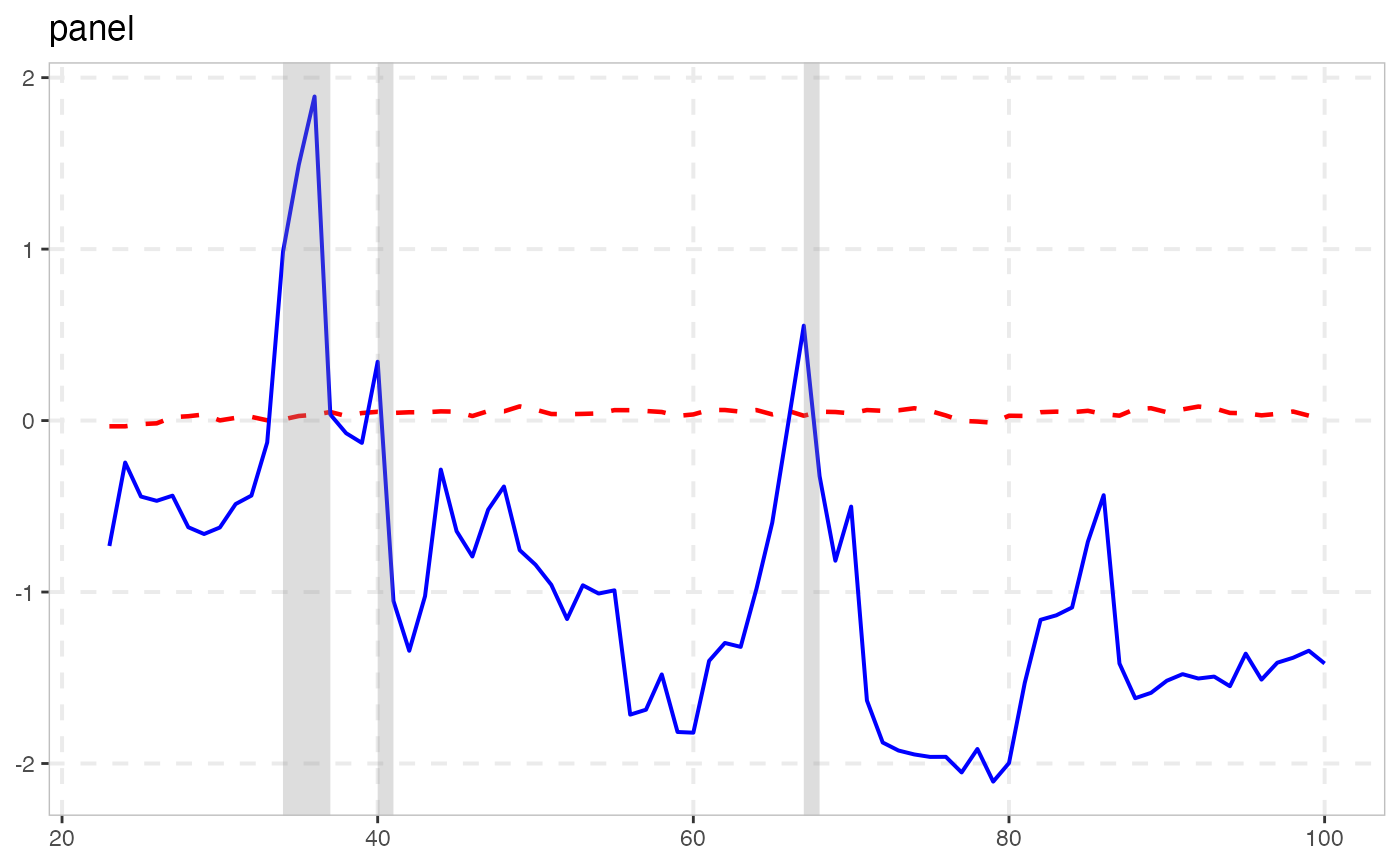

summary(rsim_data, cv = sb)

#>

#> ── Summary (minw = 19, lag = 1) ─────────────── Sieve Bootstrap (nboot = 500) ──

#>

#> panel :

#> # A tibble: 1 × 5

#> stat tstat `90` `95` `99`

#> <fct> <dbl> <dbl> <dbl> <dbl>

#> 1 gsadf_panel 1.89 0.356 0.451 0.637

#>

autoplot(rsim_data, cv = sb)

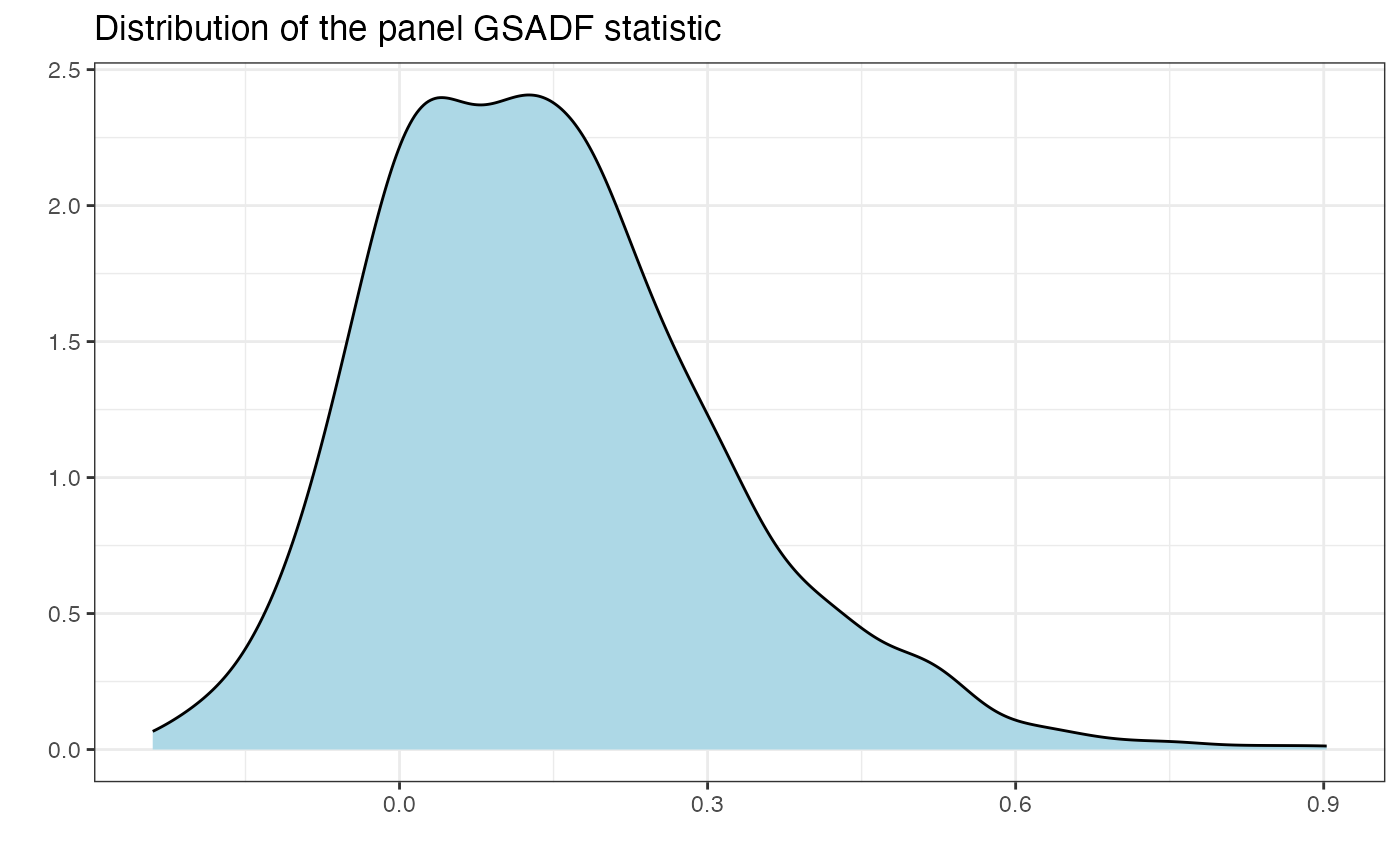

# Simulate distribution

sdist <- radf_sb_distr(sim_data, lag = 1, nboot = 1000)

autoplot(sdist)

# Simulate distribution

sdist <- radf_sb_distr(sim_data, lag = 1, nboot = 1000)

autoplot(sdist)

# }

# }